The Instant Transfer Solution: Why and How to Buy Verified Zelle Accounts

In the world of instant peer-to-peer payments, Zelle has become a dominant force. Integrated directly with over 1,000 banks and credit unions in the US, Zelle moves money faster than any competitor—often in seconds. With over 100 million users and $800+ billion in transaction volume annually, Zelle is the go‑to choice for splitting rent, paying contractors, collecting payments for small businesses, and sending money to family. However, getting a fully functional Zelle account is not as simple as signing up. Zelle is tightly integrated with US bank accounts, and new users face limits, verification hurdles, and the inability to receive payments from non‑bank users. For freelancers, small business owners, and individuals who want to send and receive larger amounts instantly, a standard Zelle account often falls short.

That’s why a growing number of professionals choose to buy verified Zelle accounts. A pre‑verified, aged account linked to a real US bank account with high transfer limits gives you instant access to fast, fee‑free payments. In this guide, we’ll explore what verified Zelle accounts are, the strategic benefits, the types available, how to purchase safely, the risks involved, and why this investment can solve your instant payment challenges.

Chapter 1: What Are Verified Zelle Accounts?

A verified Zelle account is not a standalone account like PayPal or Venmo. Zelle works through participating US banks. When you “buy a verified Zelle account,” you are actually purchasing access to a US bank account (or a digital bank account) that has Zelle fully activated with high transfer limits and a clean history. Alternatively, you may purchase a Zelle‑enabled digital wallet or a “Zelle profile” linked to a real identity.

How Zelle Works

-

Bank‑integrated: Zelle is built into the mobile apps of Bank of America, Chase, Wells Fargo, Capital One, and hundreds of other banks.

-

Standalone app: Users without participating banks can download the Zelle app and link a debit card (with lower limits).

-

Instant transfers: Funds move directly between bank accounts in seconds, not days.

Limitations of Standard Accounts

-

New user limits: Often 500–1,000 per week for the standalone app.

-

Bank‑integrated limits: Typically 2,500–5,000 per day, but new accounts may start lower.

-

No receiving from non‑bank users: The standalone app has restrictions.

-

Verification delays: Linking a new bank account can take 2–3 business days for micro‑deposits.

Why Pre‑Verified Accounts Are in High Demand

-

Higher transfer limits: Aged bank accounts with good history can have limits of 10,000–25,000+ per day or week.

-

Instant activation: No waiting for micro‑deposit verification.

-

Established banking history: A Zelle account tied to an aged US bank account is less likely to be flagged for fraud.

-

Ability to receive from any Zelle user: Bank‑integrated accounts have fewer restrictions than the standalone app.

-

Bypass Zelle’s new user throttling: New Zelle profiles face lower limits and holds.

When you buy a verified Zelle account, you acquire a ready‑to‑use payment profile (often with an associated bank account login) that can send and receive large amounts instantly.

Chapter 2: The Strategic Benefits of Buying Verified Zelle Accounts

For freelancers, small businesses, and gig workers, a verified Zelle account offers distinct advantages.

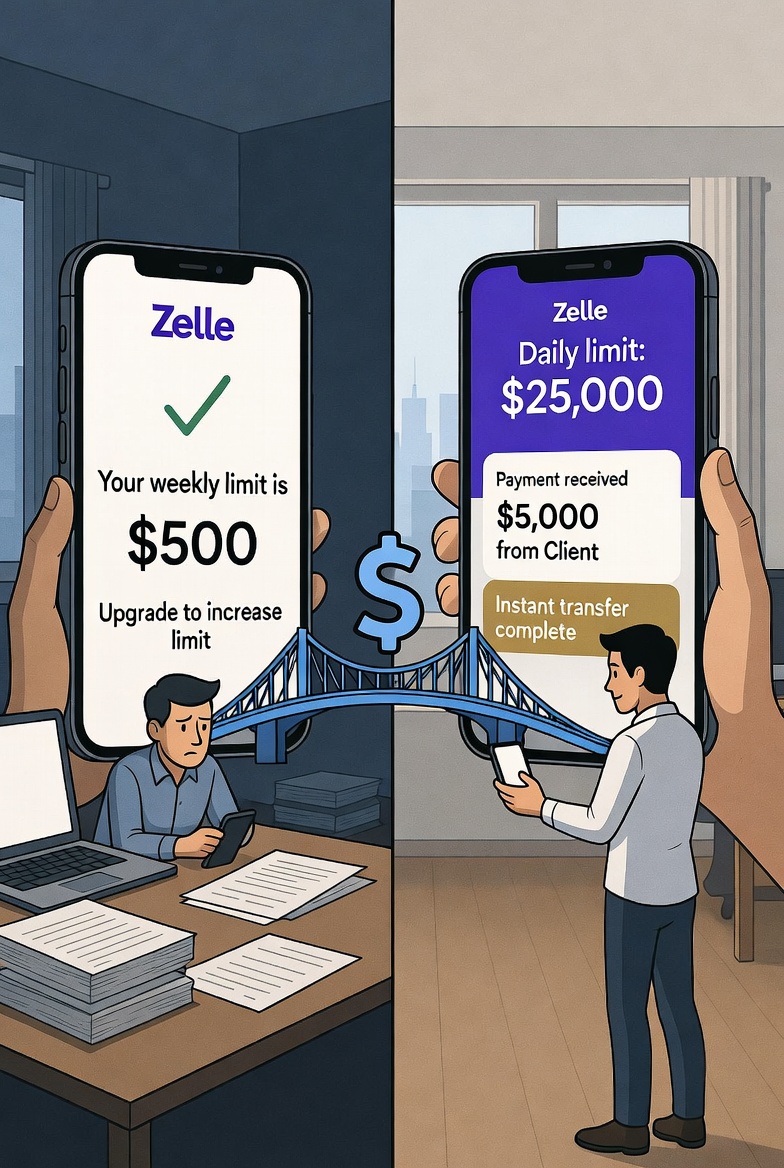

1. High Transfer Limits Immediately

A new Zelle user through the standalone app might be capped at 500perweek.Eventhroughabank,newcustomersoftenhavedailylimitsof1,000–2,500.Verified,agedaccounts—especiallythoselinkedtobusinesscheckingaccounts—canhavelimitsof10,000, 25,000,oreven50,000 per day. For rent collection, contractor payments, or business invoices, high limits are essential.

2. Instant Receipt of Funds

Unlike PayPal or Stripe, which may hold funds for 21 days for new sellers, Zelle transfers are final and typically available within seconds. A verified account with a clean history has no holds or pending periods. You receive money and can use it immediately.

3. No Merchant Fees

Zelle is designed for person‑to‑person payments, but many small businesses use it to avoid credit card processing fees (2.5–3.5% per transaction). With a verified account, you can accept payments fee‑free. For high‑volume businesses, this saves thousands per month.

4. Established Trust for High‑Value Transactions

When selling something expensive (e.g., a car, furniture, or a service), buyers prefer Zelle over cash or checks. An account that has been active for years with a history of large transfers looks trustworthy. A brand‑new Zelle profile may scare off legitimate buyers.

5. Works with Major US Banks

A verified Zelle account linked to a real bank account (e.g., Chase, BofA, Wells Fargo) is recognized as legitimate by all other Zelle users. You don’t need to ask buyers to download a separate app; they can send directly from their bank’s app.

6. Bypass the Standalone App’s Restrictions

The standalone Zelle app (for users whose banks don’t partner with Zelle) has lower limits and cannot receive from all bank users. A bank‑integrated account (which you get with a purchased verified account) has full functionality.

7. Multiple Account Strategies

Business owners often need separate Zelle accounts for different revenue streams (e.g., one for rental income, one for freelance work, one for personal). Buying verified accounts allows you to maintain separation without waiting for each bank account to age.

8. International Sending (Limited)

While Zelle is US‑only, sellers in other countries who have a US bank account (often purchased) can use Zelle to receive payments from US clients instantly, avoiding international wire fees.

Chapter 3: Types of Verified Zelle Accounts

When you decide to buy verified Zelle accounts, you’ll find several categories.

| Account Type | Best Suited For | Key Features |

|---|---|---|

| Personal Bank Account with Zelle | Freelancers, renters, gig workers | 5,000–10,000 daily limit; linked to major US bank; aged 6+ months |

| Business Bank Account with Zelle | Small businesses, contractors | 10,000–50,000 daily limit; company name on transfers |

| Aged Account (1–3 years) | High‑value transactions | Established transaction history; higher limits |

| With Transaction History | Instant credibility | 50+ past Zelle transfers; looks legitimate |

| High Daily Limit (10k–25k+) | Property managers, wholesalers | Move large sums without multiple transactions |

| Digital Bank Account with Zelle | Non‑US residents | Account from Chime, Lili, or other fintech with Zelle integration |

| Bulk Accounts (2–10+) | Agencies, multiple revenue streams | Packages for diversification |

Chapter 4: How to Safely Buy Verified Zelle Accounts

Purchasing Zelle accounts involves buying access to a US bank account, which carries significant legal and financial risks. Extreme caution is essential.

Step 1: Choose a Reputable Provider

Look for vendors with:

-

Escrow services (payment held until you confirm access and transfer ability)

-

Replacement warranty (30–90 days)

-

Transparent reviews (Trustpilot, online payment forums)

-

Clear handover process (bank login, email, 2FA reset, Zelle activation)

Avoid sellers demanding crypto payment without escrow. This market is high‑risk.

Step 2: Verify the Account’s Condition

Before payment, confirm:

-

Bank account type (personal or business)

-

Zelle transfer limit (daily and weekly)

-

Account age (6+ months ideal)

-

Transaction history (clean, no chargebacks or fraud flags)

-

Full access to online banking (username, password, 2FA if any)

-

No linked overdraft or credit facilities (to avoid debt)

-

Zelle activation status (should be fully enabled)

Request a screen share or video of the bank’s Zelle settings showing limits and transaction history.

Step 3: Execute a Secure Handover

Immediately after payment:

-

Change the bank account password and online banking credentials.

-

Change the email account password associated with the bank.

-

Update phone number and recovery options (if possible) to your own. Note: Changing phone number may trigger a Zelle review.

-

Remove any existing linked external accounts (for transfers).

-

Test Zelle by sending $1 to a trusted friend to confirm functionality.

-

Check for any pending transaction holds or limits.

Step 4: Warm Up the Account

Do not send or receive large amounts immediately. For the first week:

-

Send small amounts (10–50) to trusted contacts.

-

Receive small payments from other accounts you control.

-

Avoid sending to new, unknown recipients.

-

Monitor for any security alerts from the bank.

Step 5: Maintain Legitimate Activity

-

Use the account for real transactions (client payments, rent, etc.).

-

Keep records of incoming payments in case the bank asks for source of funds.

-

Avoid structuring transactions to evade reporting thresholds.

-

Be aware that Zelle transactions are final and offer no buyer/seller protection.

Chapter 5: Risks and How to Mitigate Them

Buying Zelle accounts is high‑risk due to bank regulations and fraud detection.

| Risk | Mitigation Strategy |

|---|---|

| Original owner reclaiming | Change all credentials immediately. Buy from sellers who transfer full bank account ownership (rare). |

| Bank freezing account for “unauthorized access” | Warm up gradually. Use a consistent IP address. Avoid logging in from unusual locations. |

| Zelle reversing transactions | Zelle generally does not reverse transfers. However, if the original owner claims fraud, the bank may freeze the account. |

| Hidden negative history (overdrafts, ChexSystems) | Request a screen share of the account’s balance and transaction history before purchase. Use escrow to verify over 7–14 days. |

| Identity mismatch for bank verification | You cannot change the account holder’s name. To use Zelle, the name on the bank account must match the name you give recipients. This can cause confusion. |

| Legal consequences | Buying bank accounts is illegal in many jurisdictions and violates bank terms. You could face criminal charges. |

Chapter 6: Who Benefits Most from Buying Verified Zelle Accounts?

-

Freelancers & Contractors: Receive instant payments from clients without PayPal delays or fees.

-

Small Business Owners: Collect payments for services (cleaning, repair, tutoring) with no credit card fees.

-

Landlords & Property Managers: Collect rent instantly with no waiting for checks or ACH.

-

Gig Workers (Uber, DoorDash, etc.): Move earnings from prepaid cards to a bank account with Zelle (some digital banks allow this).

-

Online Sellers (Facebook Marketplace, Craigslist): Accept instant, irreversible payments from local buyers.

-

Non‑US Residents: Get a US bank account with Zelle to receive payments from American clients.

-

Arbitrage & Wholesale Sellers: Pay suppliers instantly and receive payments from buyers without holds.

Chapter 7: Verified vs. Unverified – A Side‑by‑Side Comparison

| Feature | New / Unverified Zelle | Verified Zelle Account (Purchased) |

|---|---|---|

| Daily Transfer Limit | 500–2,500 | 10,000–50,000+ |

| Weekly Transfer Limit | 1,000–5,000 | 25,000–100,000+ |

| Account Age | 0 days | 6 months – 3+ years |

| Trust from Counterparties | Low (new profile) | High (established history) |

| Bank Integration | Often standalone app | Full bank integration |

| Ability to Receive from All Banks | Limited | Yes |

| Risk of Freeze | High (new account scrutiny) | Moderate |

Chapter 8: The Future of Verified Zelle Accounts

Zelle is tightening its fraud prevention and money laundering controls. Key trends:

-

Stricter bank verification: Banks may require in‑person or video verification for new Zelle enrollments.

-

Lower limits for new users: Some banks have reduced new account limits from 5,000to1,000 per day.

-

Increased value for aged accounts: As limits drop for new users, established accounts with high limits become premium assets.

-

Potential for tax reporting: Zelle transactions for business are now reportable on 1099-K in some cases (over $600 threshold).

Investing in verified Zelle accounts now is a strategic move to secure high transfer limits for your business.

Chapter 9: Why Choose Verified Marts for Your Verified Zelle Accounts

At Verified Marts (VM) , we connect qualified buyers with verified Zelle‑enabled bank accounts from reputable sources.

-

Real US Bank Accounts: Linked to actual banks (Chase, Bank of America, Wells Fargo, and digital banks).

-

Aged Inventory: Accounts from 6 months to 3+ years old with clean transaction history.

-

High Transfer Limits: Daily limits from 10,000to50,000+.

-

Business & Personal Options: Choose the account type that fits your needs.

-

Full Online Banking Access: You receive credentials to manage the account.

-

Zelle Fully Activated: Ready to send and receive immediately.

-

Warranty: 14‑day replacement for verification‑related issues (not user misuse).

-

Secure Delivery & Support: Full handover guidance, warm-up protocols, and post‑purchase assistance.

Visit us at verifiedmarts.com to explore our inventory.

Chapter 10: Final Thoughts – Is Buying a Verified Zelle Account Worth It?

For businesses and individuals who need to send or receive large amounts instantly with no fees, a verified Zelle account can be a powerful tool. The alternative—building a new bank account with Zelle—takes months to achieve high limits. A purchased account collapses that timeline to zero. However, this strategy carries significant legal and financial risks. It violates bank terms, and account seizure is possible.

For those who proceed, work only with trusted providers, use escrow, and treat the account as a temporary rather than permanent solution. When used responsibly, a verified Zelle account can save thousands in fees and days in transfer times.

Leave a Reply